Kennesaw’s Ashford Capital Partners’ Managing Partner Matthew Riedemann brings you news you can use.

Pending home sales for the month of April plummeted 9.2% compared to April 2013, the National Association of Realtors reported Thursday.

Contracts signed to buy existing homes increased 0.4% in April compared to March 2014, but that’s coming off three months of flat sales blamed on cold weather.

The expectation had been for at least a 2% gain month-over-month.

Optimistic economists expected that there was a swathe of pent-up demand that would flood the market at the start of the spring buying season. That didn’t happen.

“Higher inventory levels are giving buyers more choices, and a slight decline in mortgage interest rates this spring is raising prospective homebuyers’ confidence,” said Lawrence Yun, chief economist for the NAR. “An uptrend in closed sales is expected, although some months will encounter a modest setback.”

Sales have arrested despite mortgage rates now being at a near nine-month low after five straight weeks of steady declines. The 30-year fixed rate mortgage this week was 4.12%. Even refinancings have dropped to 37% of all mortgage activity, meaning borrowers are staying away despite historic lows.

Which means it could get worse, as Yun projects the 30-year fixed-rate mortgage to trend up and average 5.5% next year.

“The extent to which higher mortgage interest rates will impact housing affordability and sales depends on income growth, ongoing improvement in the labor market and any change to mortgage underwriting conditions,” he said.

This comes as the economy is looking at more bad news.

The nation’s domestic economic output for the first quarter was revised downward Thursday, posting a contraction of -1.0% from a meager positive 0.1% initially reported.

This was the first gross domestic product contraction since the first quarter of 2011, the Bureau of Economic Analysis reported. (GDP is the output of goods and services produced by labor and property located in the United States.)

In the fourth quarter, real GDP increased 2.6%.

The decrease in real GDP in the first quarter included declines in residential fixed investment spending. The balance was negative contributions from private inventory investment, exports, nonresidential fixed investment, and state and local government spending.

Kennesaw’s Ashford Capital Partners’ Managing Partner Matthew Riedemann brings you news you can use. The Federal Housing Finance Agency (FHFA) released its latest Refinance Report, looking at data from the first quarter of 2014. The government agency reported that in Q1 2014, approximately 77,000 refinances were completed through the Home Affordable Refinance Program (HARP), bringing the total refinances through HARP to 3.1 million since the program’s inception.

Total refi volume decreased in March, dropping to levels last seen in 2008. HARP was initially set to expire on December 31, 2013, but was extended to expire on December 31, 2015 in order to continue helping homeowners underwater on their mortgage.

The first quarter of 2014 marks the fourth straight quarter that total refinances and HARP refinances have declined. The report attributed the decline in refi’s to March’s rising interest rates.

The total volume of HARP refinances was 21 percent of all refinances for the quarter, with 12 percent of loans refinanced through HARP with a loan-to-value ratio greater than 125 percent.

In the first quarter of 2014, 23 percent of HARP refinances for underwater borrowers were for shorter-term, 15- and 20- year mortgages. The remaining 77 percent of loans were for the longer, more traditional 30-year note.

According to the FHFA, borrowers who refinanced through HARP had a lower delinquency rate compared to borrowers eligible for HARP who did not use the program.

“Year-to-date through March 2014, HARP refinances represented 41 percent of total refinances in Georgia and 38 percent of the total refinances in Florida, nearly double the 21 percent of total refinances nationwide over the same period,” FHFA said.

Other notable states with a large percentage of HARP refinances as a percentage of total refinances include Nevada (33 percent), Michigan (33 percent), and Illinois (31 percent).

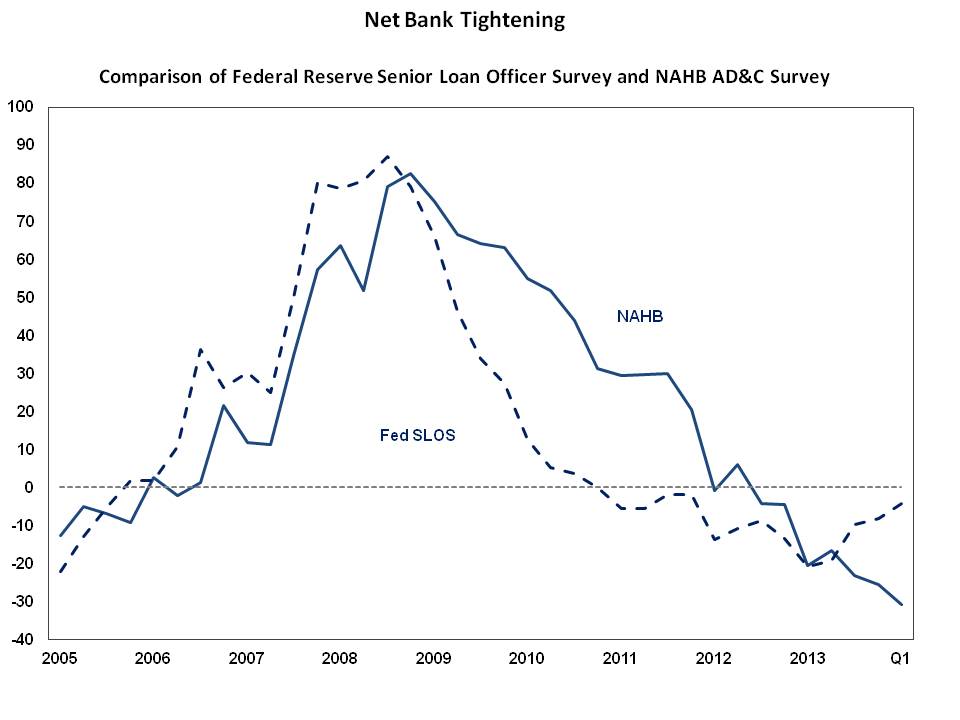

Kennesaw’s Ashford Capital Partners’ Managing Partner Matthew Riedemann brings you news you can use.

Builders and developers continue to report easing credit conditions for acquisition, development, and construction (AD&C) loans according to NAHB’s survey on AD&C financing.

In the first quarter of 2014, the overall net tightening index based on the AD&C survey improved (i.e., declined) from -25.5 to -30.8. The index is constructed so negative numbers indicate easing of credit; positive tightening, so a lower negative index means greater easing. Meanwhile, a similar net tightening index from the Federal Reserve’s survey of senior loan officers edged up from -8.1 to -4.2. This is the third consecutive quarter that the two indices moved in opposite directions.

According to the NAHB survey, less than 15% of respondents report credit conditions worsening in the first quarter. For example, only 6% of NAHB members said availability of credit for land acquisition had gotten worse, compared to 33% who said it had improved.

Only 5% reported worsening credit conditions for single-family construction, compared to 46% who reported better conditions. Similarly, only 5% and 13%, respectively, said credit available for land development and multifamily construction was worse during the first quarter of 2014.

Among members who reported tighter credit conditions in the first quarter, the most common problems were requiring personal guarantees or collateral not related to the project (60%), reducing the amount they are willing to lend (55%), lenders simply not making new loans and lowering the allowable LTV (or loan-to cost) ratio (50% each).

Although commercial banks remain the primary source of credit for AD&C by a wide margin, private individual investors have emerged as a viable alternative, especially for A&D loans. Private investors were the primary source of land acquisition loans for 25% of NAHB members, of land development loans for 11%, and for single-family construction loans for 9%. For A&D loans, private individual investors were the second most common source of credit (they were third most common for single-family construction after thrift institutions). The second most common source of multifamily construction loans was housing finance agency programs (17%).

The percentages of builders and developers putting projects on hold until the financing climate improves were slightly higher than in the fourth quarter 2013. For land acquisition, the share putting projects on hold increased from 27% to 32%; for land development, the share increased from 27% to 31%; and for single-family construction, it went up from 17% to 20%. For multifamily construction, the share putting projects on hold increased from 13% in the fourth quarter of 2013 to 23% in the first quarter of 2014.

Kennesaw’s Ashford Capital Partners’ Managing Partner Matthew Riedemann brings you news you can use. Case-Shiller shares with us.

Home prices continued to ascend through the end of the first quarter, though increases slowed down to match other weak indicators.

The S&P/Case-Shiller Home Price Indices, released Tuesday, recorded a seasonally adjusted 1.2 percent monthly rise in prices across 20 of the country’s top markets. Removing adjustments, the index climbed 0.9 percent month-over-month.

A consensus forecast from economists surveyed by Econoday called for an adjusted monthly increase of 0.7 percent.

Compared to a year ago, March prices were up 12.4 percent, a step back from the 12.9 percent annual increase recorded in February.

“The year-over-year changes suggest that prices are rising more slowly,” said David M. Blitzer, chairman of the Index Committee at S&P Dow Jones Indices. “Annual price increases for the two Composites have slowed in the last four months and 13 cities saw annual price changes moderate in March.”

Despite decelerating price growth, all cities in the composite index posted higher prices than a year ago, and four locations—Boston, Charlotte, Portland, and San Francisco—are now within 15 percent of their previous peaks. Denver and Dallas, which recovered to their perspective peaks months ago, continue to push up, meanwhile.

The latest index release also included quarterly data, showing prices rising 0.2 percent quarter-to-quarter in Q1. Compared to last year, prices were up 10.3 percent.

Looking at other market indicators, Blitzer says the picture “remain[s] mixed.”

“April housing starts recovered the drop in March but virtually all the gain was in apartment construction, not single family homes,” he said. “New home sales also rebounded from recent weakness but remain soft.”

At the same time, he added, “Other comments include arguments that student loan debt is preventing many potential first time buyers from entering the housing market.”

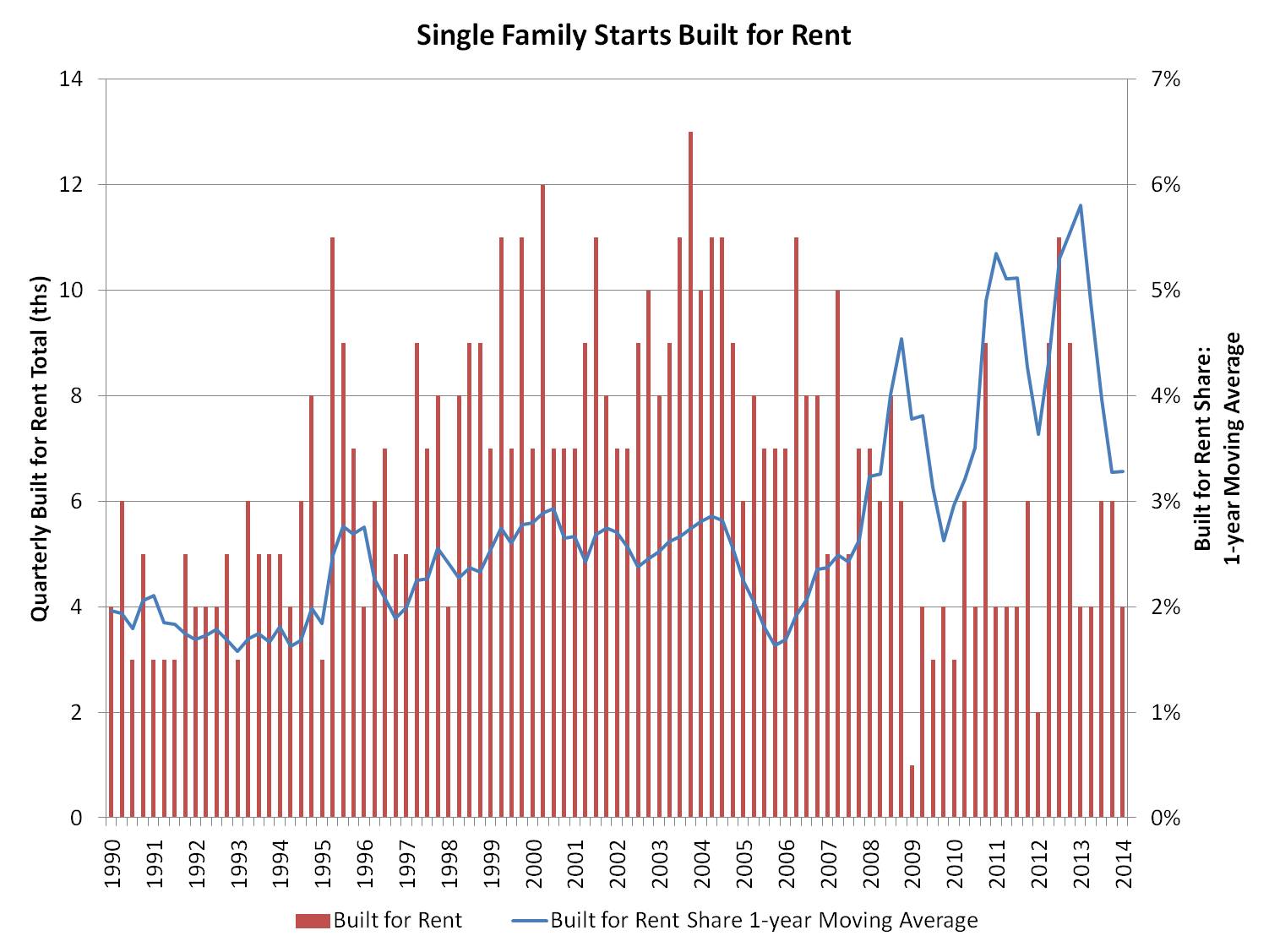

Kennesaw’s Ashford Capital Partners’ Managing Partner Matthew Riedemann brings you news you can use.

Single-family starts built-for-rent were effectively unchanged at 4,000 starts for the first quarter of 2014. While the market share of built-for-rent single-family units remains elevated, the share and count of starts appear to be declining off post-Great Recession highs.

According to data from the Census Bureau’s Quarterly Starts and Completions by Purpose and Design and NAHB analysis, the market share of single-family homes built-for-rent, as measured on a one-year moving average, stands at 3.3% for the first quarter of 2014. This remains higher than the historical average of 2.8% but is down from the 5.8% registered a year ago.

With the onset of the Great Recession, the share of built-for-rent homes rose, with a dip in the percentage during the homebuyer tax credit period.

Despite the elevated market concentration, the total number of single-family starts built-for-rent remains fairly low – only 20,000 homes started during the last four quarters. It appears the market is returning to historical averages after recent peaks in this form of construction.

Kennesaw’s Ashford Capital Partners’ Matthew Riedemann brings you news you can use.

For the first third of this decade, big city population growth continues to outpace the rates of 2000 through 2010, according to new data released by the Census Bureau. It raises the question: Is this city growth revival here to stay? Or, is it a lingering symptom of the recession, mortgage meltdown and the plight of still stuck in place young adults? The new statistics, which update city populations through July 2013, give some credence to both theories.

On the positive side for urban boosters, the numbers show that many cities have gained more people in the three-plus years since the 2010 Census than they gained for the entire previous decade. This includes three of the five largest cities, New York, Philadelphia and Chicago (which lost population in the previous decade). Among the 25 largest cities, nine are already ahead of their previous decade’s gains, including Dallas, Denver, Memphis, San Francisco, San Jose and Washington, D.C. (See table)

Still another positive indicator for big cities is their growth rates. For each of the last three years, cities with populations exceeding 250,000 grew at rates exceeding 1 percent—far higher than their average annual rate of 0.49 percent over the 2000-2010 decade (Figure 1). Among the fastest growing, with rates exceeding 2 percent are Seattle, Austin, Charlotte, Denver and Washington D.C., each with new knowledge based economies and high amenity downtowns.

Figure 1: Large City Growth*

Yet, despite the overall gains, growth rates slowed in the most recent year for 45 of the 77 cities over 250,000 in population, but for the most part, the growth rate declines were less than 0.5 percent

In the city versus suburb realm, the new numbers once again affirm a reversal that counters decades of suburban-dominated regional growth among metro areas with more than 1 million people. Now, for three years running, primary cities are growing faster than their suburbs (See Figure 2).

From 2000 to 2010 as with many prior years, suburban growth substantially exceeded that of primary cities. This changed in the each of the three subsequent years. In 2012-2013, 19 of the 51 major metropolitan areas showed faster primary city than suburb growth including New York, Washington D.C., Denver and Seattle. (See table)

Figure 2: City and Suburb Growth Reversals*

Still, the new numbers for 2012-13, suggest a closing of the city-suburb growth gap with the small downtick in city growth and an even tinier suburban growth uptick. This modest suburban growth rise is reinforced by a separate updated analysis of exurban counties that showed their population growth rise from a low 0.4 percent in 2011-2012 to 0.6 percent in 2012-2013. This is still well below the exurban growth rates of around 2 percent during the high suburbanization years in the middle of last decade.

So where are cities headed for the rest of the decade? This initial city growth upsurge could well be attributable to recession’s aftermath and the suburban housing market slowdown. If that were the case, then the newly reported city growth slowdown and modest exurban gains could signal that past suburban growth patterns are re-emerging.

Yet city growth levels remain strong by the standards of recent history. Moreover, the cities that are growing most rapidly are located in areas with economies and amenities that are attractive to millennials, graduates and young professionals, who make up a growing portion of potential movers. So while it is too soon to anoint this the “decade of the city,” the persistence of big city growth is hard to ignore.

President Barack Obama officially nominated San Antonio Mayor Julián Castro to lead the U.S. Department of Housing and Urban Development in a ceremony on Friday afternoon. “I am nominating another all-star who’s done a fantastic job in San Antonio over the last five years,” Obama said.

The other all-star that the President was referring to is Shaun Donovan, the current HUD secretary.

Donovan has been a member of President Obama’s cabinet since Obama took office in 2008. “When we took office in 2008, every member of my cabinet had a tough job in front of them,” Obama said Friday. “Few had a tougher job that Shaun Donovan. Five years later, things look a lot different. But we’re not anywhere close to where we need to be yet.”

Obama noted the “millions of families that have been able to come up for air” during Donovan’s tenure of HUD. “Over the years, Shaun has taken an agency with a $40 billion budget and made it smarter and more efficient,” Obama said. “He’s helped build strong sustainable neighborhoods. He’s helped 4.3 million families buy their piece of the American dream.”

Citing Donovan’s “outstanding work” during his time at HUD, President Obama nominated Donovan to the post of Director of the Office of Management and Budget, which opened the post for Castro. “I’m absolutely confident that he’ll do a great job as head of OMB,” Obama said.

“We also need someone to continue Shaun’s good work at HUD,” the President said. “And that public servant is Julián Castro.”

Obama joked that many Americans became familiar with the “good-looking” Castro during the 2012 Democratic National Convention. The President also joked that Castro was a “pretty good speaker,” perhaps in a nod to the two men’s similarities as charismatic public speakers.

“He’s been focused on revitalizing one of our greatest cities and has become a leader in housing and economic development,” Obama said of Castro.

Castro, the three-term mayor of San Antonio, called the nomination “quite an honor” in his remarks. “To be your nominee is simply a blessing,” Castro said. “I stand of the shoulders of so many folks of the past generations.”

Castro cited his and his brother’s experience going from growing up in rental housing in San Antonio to eventually becoming nationally known public servants as something that gave the brothers a “sense of what’s possible.”

Castro’s twin brother Joaquin now represents Texas’s 20th District in the U.S. House of Representatives.

Castro also said that “we are in a century of cities” and said that housing was “at the top of the agenda” going forward. “We need to ensure that we have good, safe, affordable housing for everyone so they can all achieve their American dreams,” Castro said.

Donovan thanked the “outstanding team” at HUD for their work in his time as HUD secretary. “The HUD team is made up of extraordinary public servants,” Donovan said.

Donovan called himself a “numbers guy” who often asks to see spreadsheets that his colleagues at HUD are reviewing. “I’m happy to go to a place where my love of spreadsheets will be embraced,” he said.

President Obama said that he is hoping for a “quick confirmation” for both Donovan and Castro. “I hope that the Senate confirms them both without games or delay,” he added.

Prior to Castro’s official nomiation, analysts from Compass Point said that they did not anticpate a strategic shift when Castro takes over at HUD. “Our conversations lead us to believe that Castro is unlikely to deviate materially from the existing FHA single-family strategy,” said Compass Point analyst Isaac Boltansky. “The potential impact of the leadership change at HUD is admittedly an unknown at this junction but there is little reason – either political or fundamental – to expect a MIP reduction prior to 2015.”

The National Association of Home Builders greeted Castro’s nomination positively. “NAHB congratulates Mayor Castro on his nomination as HUD secretary,” said Kevin Kelly, chairman of the NAHB. “Upon his confirmation to the Cabinet post, NAHB looks forward to working with Mr. Castro to promote policies that will ensure stable and liquid mortgage markets for single-family and multifamily housing and to address the many challenges that face our industry, including persistently tight credit conditions that are preventing qualified buyers from obtaining home loans.”

Castro’s nomination was also welcomed by the National Council of La Raza, whose president and CEO Janet Murguía, said, “As we have said, the president hit a home run with this nomination. Julian Castro has become a respected and nationally acclaimed leader on urban revitalization and economic development, the issues at the heart of the Department of Housing and Urban Development’s work.

“We especially look forward to working with him to complete the department’s unfinished business of alleviating once and for all the housing crisis that continues to affect millions of Americans, especially in communities of color.”

Three years after the Civil War ended, on May 5, 1868, the head of an organization of Union veterans — the Grand Army of the Republic (GAR) — established Decoration Day as a time for the nation to decorate the graves of the war dead with flowers. Maj. Gen. John A. Logan declared that Decoration Day should be observed on May 30. It is believed that date was chosen because flowers would be in bloom all over the country.

The first large observance was held that year at Arlington National Cemetery, across the Potomac River from Washington, D.C.

The ceremonies centered around the mourning-draped veranda of the Arlington mansion, once the home of Gen. Robert E. Lee. Various Washington officials, including Gen. and Mrs. Ulysses S. Grant, presided over the ceremonies. After speeches, children from the Soldiers’ and Sailors’ Orphan Home and members of the GAR made their way through the cemetery, strewing flowers on both Union and Confederate graves, reciting prayers and singing hymns.

Local Observances Claim To Be First Local springtime tributes to the Civil War dead already had been held in various places. One of the first occurred in Columbus, Miss., April 25, 1866, when a group of women visited a cemetery to decorate the graves of Confederate soldiers who had fallen in battle at Shiloh. Nearby were the graves of Union soldiers, neglected because they were the enemy. Disturbed at the sight of the bare graves, the women placed some of their flowers on those graves, as well.

Today, cities in the North and the South claim to be the birthplace of Memorial Day in 1866. Both Macon and Columbus, Ga., claim the title, as well as Richmond, Va. The village of Boalsburg, Pa., claims it began there two years earlier. A stone in a Carbondale, Ill., cemetery carries the statement that the first Decoration Day ceremony took place there on April 29, 1866. Carbondale was the wartime home of Gen. Logan. Approximately 25 places have been named in connection with the origin of Memorial Day, many of them in the South where most of the war dead were buried.

Official Birthplace Declared In 1966, Congress and President Lyndon Johnson declared Waterloo, N.Y., the “birthplace” of Memorial Day. There, a ceremony on May 5, 1866, honored local veterans who had fought in the Civil War. Businesses closed and residents flew flags at half-staff. Supporters of Waterloo’s claim say earlier observances in other places were either informal, not community-wide or one-time events.

By the end of the 19th century, Memorial Day ceremonies were being held on May 30 throughout the nation. State legislatures passed proclamations designating the day, and the Army and Navy adopted regulations for proper observance at their facilities.

It was not until after World War I, however, that the day was expanded to honor those who have died in all American wars. In 1971, Memorial Day was declared a national holiday by an act of Congress, though it is still often called Decoration Day. It was then also placed on the last Monday in May, as were some other federal holidays.

Some States Have Confederate Observances Many Southern states also have their own days for honoring the Confederate dead. Mississippi celebrates Confederate Memorial Day on the last Monday of April, Alabama on the fourth Monday of April, and Georgia on April 26. North and South Carolina observe it on May 10, Louisiana on June 3 and Tennessee calls that date Confederate Decoration Day. Texas celebrates Confederate Heroes Day January 19 and Virginia calls the last Monday in May Confederate Memorial Day.

Gen. Logan’s order for his posts to decorate graves in 1868 “with the choicest flowers of springtime” urged: “We should guard their graves with sacred vigilance. … Let pleasant paths invite the coming and going of reverent visitors and fond mourners. Let no neglect, no ravages of time, testify to the present or to the coming generations that we have forgotten as a people the cost of a free and undivided republic.”

The crowd attending the first Memorial Day ceremony at Arlington National Cemetery was approximately the same size as those that attend today’s observance, about 5,000 people. Then, as now, small American flags were placed on each grave — a tradition followed at many national cemeteries today. In recent years, the custom has grown in many families to decorate the graves of all departed loved ones.

The origins of special services to honor those who die in war can be found in antiquity. The Athenian leader Pericles offered a tribute to the fallen heroes of the Peloponnesian War over 24 centuries ago that could be applied today to the 1.1 million Americans who have died in the nation’s wars: “Not only are they commemorated by columns and inscriptions, but there dwells also an unwritten memorial of them, graven not on stone but in the hearts of men.”

To ensure the sacrifices of America ’s fallen heroes are never forgotten, in December 2000, the U.S. Congress passed and the president signed into law “The National Moment of Remembrance Act,” P.L. 106-579, creating the White House Commission on the National Moment of Remembrance. The commission’s charter is to “encourage the people of the United States to give something back to their country, which provides them so much freedom and opportunity” by encouraging and coordinating commemorations in the United States of Memorial Day and the National Moment of Remembrance.

The National Moment of Remembrance encourages all Americans to pause wherever they are at 3 p.m. local time on Memorial Day for a minute of silence to remember and honor those who have died in service to the nation. As Moment of Remembrance founder Carmella LaSpada states: “It’s a way we can all help put the memorial back in Memorial Day.”

New York and L.A. are losing more Americans than they’re gaining, but the flood of immigrants more than makes up for it.

America’s largest metro areas, which are currently gaining population at impressive rates, are driving much of the population growth across the nation. But that growth is the result of two very different migrations – one coming from the location choices of Americans themselves, the other shaped by where new immigrants from outside the United States are heading.

Working closely with demographer and Martin Prosperity Institute colleague Karen King, I decided to take a closer look at newly released data from the U.S. Census Bureau, which breaks out metro population growth according to its various components. We looked at domestic migration; international migration; and net migration for 2012 to 2013. MPI’s Zara Matheson mapped the patterns.

While many metro areas are attracting a net-inflow of migrants from other parts of the country, in several of the largest metros – New York, L.A., and Miami, especially – there is actually a net outflow of Americans to the rest of the country. Immigration is driving population growth in these places. Sunbelt metros like Houston, Dallas, and Phoenix, and knowledge hubs like Austin, Seattle, San Francisco, and D.C. are gaining much more from domestic migration.

Most large metros, those with at least a million residents, had more people coming in than leaving. As I noted last month, the metros with the highest levels of population growth due to migration are a mix of knowledge-based economies and Sunbelt metros, including Houston, Dallas, Miami, D.C., San Francisco, Seattle, and Austin.

Eleven large metros, nearly all in or near the Rustbelt, had a net outflow of migrants, including Chicago, Detroit, Memphis, Philadelphia, and St. Louis. (Many of these metros still saw their overall populations grow due to “natural increase,” as birth rates outstripped death rates.

All large metros had a net inflow of immigrants. The metro that attracted the most immigrants was, unsurprisingly, New York, with a net-inflow of 128,000 individuals. Next in line is Miami, with nearly 53,000 immigrants, and Los Angeles, with nearly 50,000. Washington, D.C., attracted nearly 37,000 immigrants, while Houston, Boston, Chicago, and San Francisco each attracted between 20,000 and 30,000. Dallas, Philadelphia, Seattle, Atlanta, Orlando, San Jose, San Diego, Minneapolis, and even Detroit attracted between 10,000 and 20,000 immigrants.

The large metros with the smallest inflows of immigrants were mainly those with populations of between one and two million. These metros, including Grand Rapids, Birmingham, Memphis, Louisville, and Milwaukee, generally saw a net in-migration of somewhere between 1,000 and 3,000 immigrants.

The three largest metros – New York, Los Angeles, and Chicago – all lost Americans to the rest of the country. New York saw a net outflow of more than 100,000 from 2012 to 2013. Los Angeles and Chicago each saw a net outflow of roughly 50,000.

The biggest net gainers of domestic population were a mix of low-cost Sunbelt metros like Phoenix, San Antonio, Dallas and Orlando; energy centers like Houston; leading knowledge and technology hubs like San Francisco, Austin, and Seattle; and Nashville, with its thriving music scene. The presence of San Francisco on this list, with a net influx of nearly 17,000 Americans, is especially surprising given its high costs of living.

What’s even more interesting is that about a third of all large metros saw a net outflow of domestic migrants. These metros are a diverse bunch, including America’s three largest city-regions, New York, L.A., and Chicago; expensive, high-tech powerhouses like San Jose and San Diego; and unsurprisingly, large swaths of the Rustbelt, including Detroit, St. Louis, and Milwaukee.

The table below compares the components of net migration – overall migration, domestic migration, and international migration – for America’s ten largest metro areas.

Notice the opposite directions of the domestic and international migration patterns in several metros, including New York, Los Angeles, Chicago, Philadelphia, and Miami. The huge net influx of immigrants into New York, Los Angeles, and Miami offset the net exodus of American residents, but in Chicago and Philadelphia huge population losses to other metros led to an overall pattern of out-migration.

Some metros, in contrast, are attracting both domestic and international migrants. Houston and Dallas stand out on this score, but Atlanta is doing so as well. The knowledge economy centers of Washington, D.C. and Boston – as well as the knowledge and tech hubs of San Francisco and Austin, not on the chart above – are also attracting domestic and international migration.

These overall figures begin to paint a clearer picture of the population shifts across the U.S. But the patterns tell us little about the income, education, or skill levels of the people who are coming and going. Some of these places may be attracting higher income, higher skilled people who can afford a high cost of living, while shedding lower income, less skilled workers who are driven out by high prices. These metro-level data also tell us nothing about where different groups of people are locating, whether in the city center or the suburbs.

Kennesaw’s Ashford Capital Partners’ Matthew Riedemann brings you news you can use.

The Commerce Department released first-quarter data this morning for housing starts, permits, and completions including April readings. Jonathan Smoke, chief economist at Hanley Wood, and Brad Hunter, chief economist at Metrostudy offer market insight on the growth in single-family starts and concentration in multifamily construction in 2014 based on government and Metrostudy data.

“Metrostudy’s new field study (350 researchers drive nearly 500,000 miles every 90 days, counting all lots, starts, and units of new-home inventory) is revealing some interesting trends and turning points. Detached single-family housing starts rose by 5% comparing the first quarter of 2014 with the previous quarter, and were up by 9% compared with a year ago,” highlights Hunter.

Smoke explains the first-quarter data stating, “in the detailed quarterly permit data from the Census, all of the top 15 markets experienced growth in their three-month moving averages. Tampa was the growth leader with a 16% increase, followed by Atlanta at 14%, then Dallas and Charlotte both at 13%. Over half of the volume leaders had double-digit increases for their moving averages with five of those also showing double-digit increases from one year ago. Across all of the top fifteen for year-over-year growth, more than half also saw increases with Orlando leading at 51% over March 2013 and Chicago at 44%. Both of those markets showed a more modest 5% jump in the moving averages but significantly outperformed monthly permits in the prior year. Of the seven markets with decreases, the largest was seen in Phoenix with an 18% drop followed by Raleigh at 14%.” Housing Trends.

Smoke also highlights continued concentration of multifamily permits with 5% of MSAs making up 80% of permits for the month of March and 7% accounting for 80% of the annual volume for the most recent twelve-month period.

“The data for both single family and multifamily clearly indicate significant market variation and choppiness in activity and the overall recovery cycle, but thanks to improvement in the markets that matter most, growth appears to be the net effect. I continue to expect that the second quarter data will reveal more positive consistency as spring transitions in to summer,” explains Smoke. “I am expecting a strong second-quarter, in part because I can see that there is real growth occurring in the largest markets, through market level permit data from Census and through Metrostudy field collected starts data. Of 785 MSAs across the country included in the more detailed Census permit data, 484 or 62% demonstrated an increase in monthly single family permit volume for March 2014 over February, which is the third consecutive month with growth.”

Below are top annual volume rankings as of March 2014 by MSA:

In an interview this morning with Bob Moon on Bloomberg Radio, Hunter also noted expected growth in starts this year compared to 2013. “We’re going to see a strong year,” says Hunter. “A lot of the builders increased their prices at a 20% annualized rate in the first half of 2013. Last year builders wanted to slow down their sales based on labor supplies, lot supplies, and production…the market went backwards on them.”

Metrostudy projects an 18% growth in overall housing starts this year. “Remember, by the way, that the surge in apartments is peaking, and many of those renters are going to want to become buyers in the years ahead,” assures Hunter.

Today’s data release for new residential construction is available from the U.S. Census Bureau here.

Learn more about markets featured in this article: Atlanta, GA.

Kennesaw’s Ashford Capital Partners’ Managing Partners Matt Riedemann brings you news you can use.

Thee nationwide mortgage delinquency rate fell to an eight-year low following its largest month-over-month decline in nine years, according to Black Knight Financial Services' "First Look" at ... Read More

Kennesaw’s Ashford Capital Partners’ Managing Partners Matt Riedemann brings you news you can use.

-------

Existing-homes sales surged to their highest annual rate in 18 months, showing a promising beginning to the spring homebuying season, the latest report from the National Association ... Read More